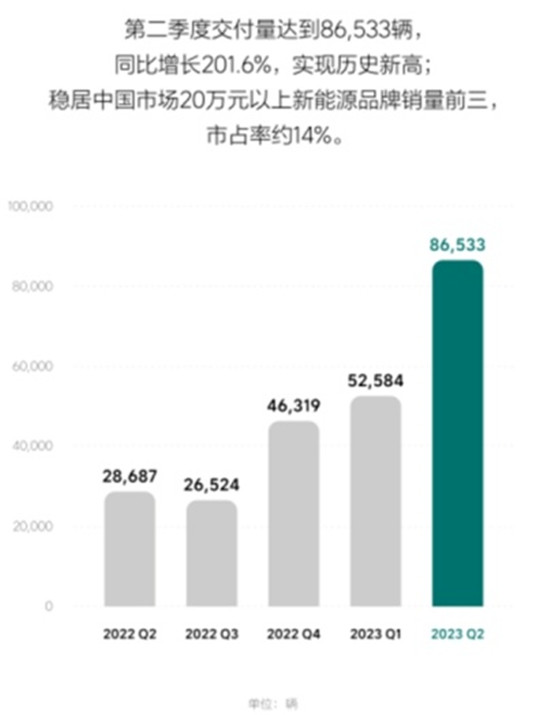

A few days ago, LI released its Q2 financial report for 2023, with revenue and delivery reaching record highs of 28.65 billion yuan and 86,533 vehicles respectively, with year-on-year growth rates exceeding 200%. In addition, the company’s operating capacity continued to improve, and Q2′ s gross profit margin increased steadily to 21.8%, making it a new force in car making and even a star in the entire automobile industry.

First, focus on the highlights in LI Q2 financial report.

In terms of financial data, LI Q2 has made a series of encouraging achievements. Revenue reached 28.65 billion yuan, a year-on-year increase of 228.1%; Operating profit and net profit both climbed, reaching 1.63 billion yuan and 2.31 billion yuan respectively; The gross profit margin increased to 21.8%, and the company’s profitability rose steadily; Free cash flow increased to 9.62 billion yuan, a substantial increase compared with the same period; By June 30, 2023, the company’s cash reserves reached 73.77 billion yuan … Both the positive and positive business trend and the ever-increasing abundant cash reserves have laid a solid foundation for the sustainable development of LI.

The strong market performance is undoubtedly one of the sources supporting LI’s good business. By the beginning of July, LI had delivered over 400,000 vehicles. From November 2019, when the first Li ONE rolled off the assembly line, to October 2021, when the 100th car rolled off the assembly line, it took 23 months. It took 10 months for 100,000 to 200,000 vehicles to go offline. From 200,000 vehicles to the cumulative delivery of more than 300,000 vehicles, it ideally took 5 months; From 300,000 vehicles to 400,000 vehicles today, the ideal took only three months, which not only explained the "ideal speed", but also highlighted the deep recognition of LI by China consumers …

At the same time, driven by the hot sales of L series models, LI also showed an accelerated expansion trend. In June, its delivery volume exceeded 30,000 vehicles for the first time, and this highlight performance continued in July; By the end of July, more than 200,000 ideal L series models had been delivered. With the release of its first all-electric flagship model MEGA approaching, LI, which has built a dual technical route of "all-electric+extended range", is worth looking forward to in the future.

LI is also favored by the capital market because of its positive circulation performance and broad prospects for development. In the first half of the year, the share price of US stocks in LI rose from $21.760/share on the first day of opening to $35.100/share on the last trading day of the first half of the year, with an increase of 61.31%. As of the release date of Q2 financial report, the closing price of LI has risen to USD 42.630/share, with a total market value of USD 44.435 billion, or about RMB 320.118 billion, and it has secured the second place in the market value of China automobile enterprises.

So, what factors have helped LI to achieve a leap-forward development?

First, LI’s precise brand positioning and product hard power, which conforms to the development of the industry and has a deep insight into the market demand. With the transformation of China’s automobile industry from big to strong, "upward" development is the only way for China’s automobile. As a "latecomer", LI lacks brand shackles and focuses on the high-end market to give it an inherent advantage; And the sweeping rise has also given it the confidence to wrestle with the traditional luxury giants, and even broken the difficulty of China brand upward.

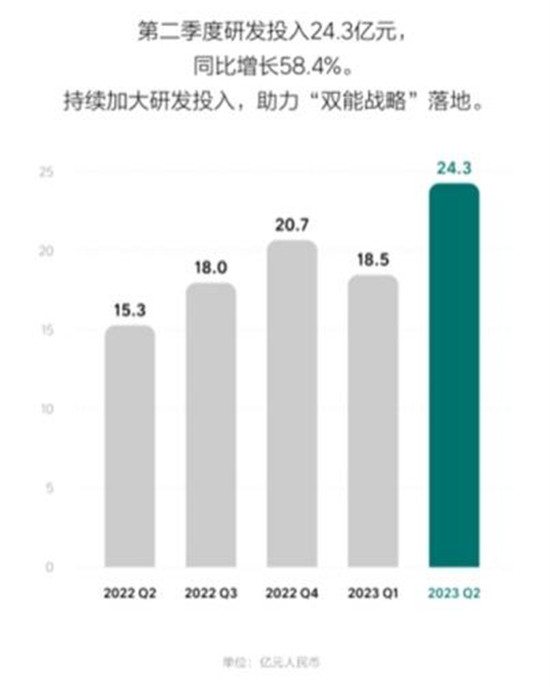

In terms of products, in view of the demand of consumers in China and the control of various market segments, the products launched by LI won the hearts of the people. The product distribution of L7, L8 and L9 meets the purchase range of most consumers. The products themselves are not only smart and comfortable configurations such as "refrigerator, sofa, big color TV" that people talk about and even change consumers’ car habits, but LI has also spent a lot of R&D investment on more cutting edges, which has effectively improved consumers’ sense of comfort in car use. For example, in the development of L-series chassis, in order to change the air suspension from the exclusive luxury car of one million to the technology that can be used by more families, LI established R&D centers in the north and south, and developed the intelligent ideal magic carpet air suspension by itself.

In addition, in order to better serve users, the network scale of stores in LI is also increasing. As of July 31, 2023, LI had 337 retail centers covering 128 cities, and operated 323 after-sales maintenance centers and authorized car body panel repair and spraying centers in 222 cities. The integration of online and offline integrated sales has promoted the improvement of sales and service efficiency.

Based on the above, LI’s unexpected market performance is also natural. More importantly, the expansion of sales volume has also brought about the appearance of scale effect: the cost of vehicle R&D and production has been greatly reduced. According to the plan, the overall R&D expenditure rate of LI will continue to be stable at around 10%, even comparable to that of large multinational automobile groups; Have more say in the supply chain, so that it has more resilience and anti-risk ability; The geometric growth of brand recognition allows it to cope with the current "price reduction tide" safely, maintaining the price and showing the brand’s strength.

The rising brand recognition, the continuous hot sale of products, the reduction of R&D costs, the upgrading of business process systems, etc., complement each other with the steady rise of the company’s operating performance, and thus form a sustainable positive cycle.

Looking ahead, whether it is the company’s own development momentum, the continuous evolution of market demand, or the overall development direction and prospects of the industry, LI will achieve a higher leap.

Personally, LI’s upcoming first pure electric vehicle will make its product matrix more perfect; Intelligent assisted driving functions such as urban NOA and commuter NOA, which will be pushed one after another, as well as vehicle capabilities that are constantly upgraded through OTA, will continuously enhance user stickiness and brand awareness; However, the company’s insistence on self-research of core technologies and increasing investment in R&D of product core technologies will become the guarantee of product hard strength.

In terms of market demand, the mid-to-high-end incremental market has gradually become the main battlefield of consumption, which coincides with the positioning of LI. Family users’ demand for car purchase is diversified, but the purpose is clear. LI L7, L8, L9 and the upcoming MEGA can fully meet the needs of various consumer groups.

From the overall prospect of the industry, new energy and high-end are also development trends. According to the data of passenger car market information association, from January to July, the total retail sales of new energy passenger cars in China reached 3.725 million, up 36.3% year-on-year. In July, the retail penetration rate of new energy passenger cars reached 36.1%.

Based on the above, it is reasonable for LI to be optimistic about the future.It is predicted that the cumulative delivery volume in the third quarter will reach 100,000 to 103,000 vehicles, up by 277.0% to 288.3% year-on-year, among which the monthly delivery volume of L8 and L9 will exceed 10,000 vehicles, and the ideal L7 will challenge the monthly delivery target of 15,000 vehicles; The quarterly revenue is expected to reach 32.33 billion yuan to 33.30 billion yuan, a year-on-year increase of 246.0% to 256.4%. In the fourth quarter, LI will deliver 40,000 vehicles a month.