Sohu’s revenue originally consisted of four parts:

1) advertising revenue. From sohu.com (including video tv.sohu.com), Focus Real Estate (Focus.cn), 17173.com (game);

2) Search (from sogou search);

3) Online games (from Changyou);

4) Mobile value-added services (from three major operators).

In the most difficult years of the "three portals", mobile value-added services have "saved the driver", but they have been shrinking in recent years. By 2013, mobile value-added revenue only accounted for 4% of Sohu’s total revenue. Since 2014, Sohu has packaged this business into the category of "other income".

See the following table for the revenue structure of Sohu (adjusted retroactively).

Changyou has already been listed, and the control right of sogou is about to fall to Tencent. Strictly speaking, Sohu’s income from these two companies belongs to "investment income" rather than operating income. In 2012, 2013 and the first half of 2014, the "investment income" of Sohu’s revenue remained above 60%, and it was already "half an investment company".

Under normal circumstances, the valuation of technology companies in the capital market is one grade higher than that of investment companies (the price-earnings ratio of Goldman Sachs is only 10 times), and Sohu’s gradual shift to investment holding is one of the reasons for the low valuation.

If Sohu is regarded as an investment company, judging from what it has done to Changyou and sogou, the two most important investment targets, Zhang Chaoyang’s idea is to "close the mountain" rather than continue to invest.!

In April 2009, Sohu Changyou was listed on Nasdaq. In July, 2013, Changyou announced that it would complete the stock repurchase worth $100 million within two years. Changyou, which is implementing the platform strategy, is at a critical moment when it needs to increase capital investment. If it encounters difficulties in refinancing, it is understandable that it is unwilling to issue shares at a "low price". It is really unreasonable to spend $100 million to buy back shares. Unless Changyou management (or Zhang Chaoyang himself) believes that this $100 million investment platform strategy will not even increase Changyou’s market value by $100 million. It is better to use it to buy back shares, which has a more direct effect on raising stock prices. At present, Sohu holds 71.75 million Changyou shares, accounting for 67.9%. Repurchase can objectively raise the price and create convenience for Sohu to reduce its holdings in the secondary market.

In October 2010, sogou, a subsidiary of Sohu, accepted an investment of $24 million from Alibaba. In June 2012, Sohu bought back the equity of sogou from Ali for US$ 25.8 million, and in September 2013, it accepted Tencent’s investment of US$ 488 million and Tencent’s Soso assets. However, this $488 million was not for sogou’s business development, of which $301 million was paid out in dividends (September 17, 2013) and $160.7 million was used to buy back shares (before July 31, 2014), and the targets of dividends and buybacks were companies controlled by Sohu and Zhang Chaoyang. After sogou was redeemed, it has been rumored that it will be sold at a "premium". Baidu and 360 Tencent are among the gossip. Zhang Chaoyang publicly stated that Sohu was not short of money and would not sell sogou. Cash out of sogou in this roundabout way.,In addition to face, there are also tax avoidance considerations.

According to the current thinking, sogou will be listed (or sold in full) only when the time is right (or the price is right). Sohu Video has long been an independent company, and it will take the road of sogou in the future. Games, search, and video services have set up their own portals, leaving only a single portal, and Sohu will be more like an investment company by then. One day, the founder will sell high-quality assets through capital operation and gradually be taken care of by professional managers. This is Zhang Chaoyang’s shrewdness, not his weakness.

Swimming is a blanket for juggling.

Although sogou has been operating independently for a long time, it lacks sufficient data to judge its influence on Sohu because it is not listed. Let’s just remove Changyou and see what the rest of the business is like.

The revenue is passable, especially in 2013, the year-on-year growth rate reached 49.3%.

But the net profit is terrible! It turns out that excluding Changyou, Sohu had a net profit of only $4 million in 2010, and lost nearly $120 million in 2012 and 2013!(Note: Sohu’s consolidation method is to merge 100% of Changyou’s game income under Online game)

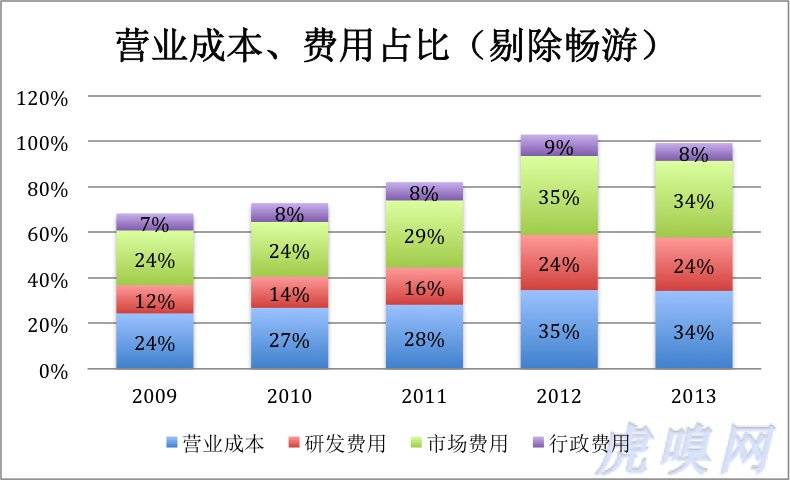

Excluding Changyou, Sohu’s business mainly includes three parts: portal, search and video. According to the data of Sina, Baidu and Youku Tudou, the gross profit margin of Sohu portal and search should be around 70%, while the video business is only around 30%. When the three businesses are mixed together, the operating cost accounts for 34% of the revenue and the gross profit rate is 66%, which is not low.

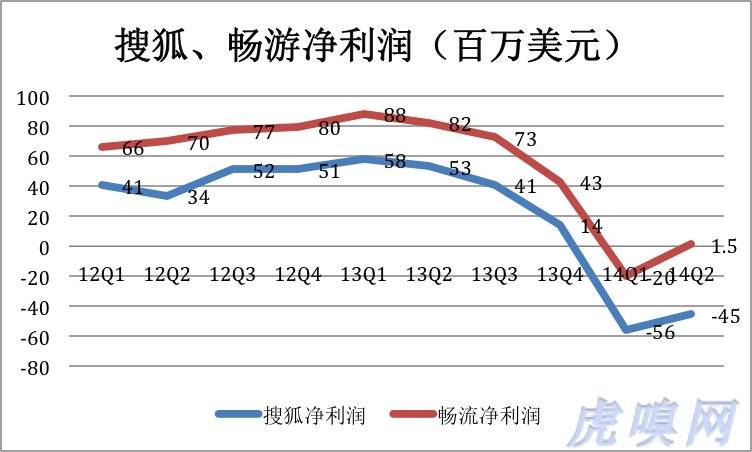

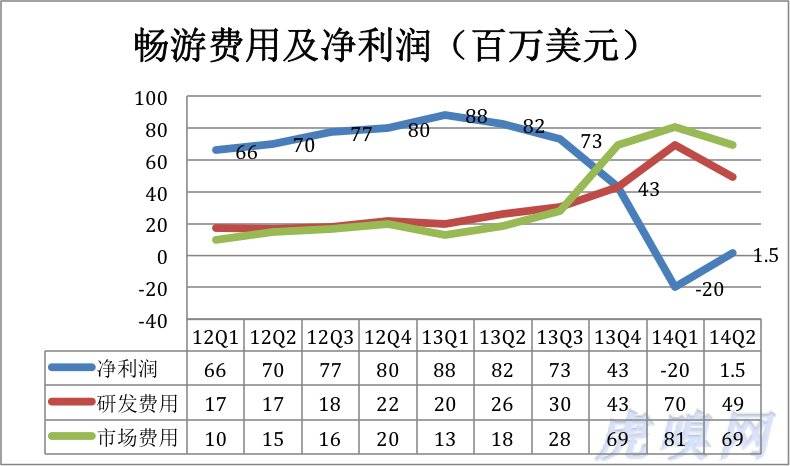

However, due to the high market expenses and R&D expenses, the final profit and loss of the above three businesses are only between the first lines.As a result, Changyou is profitable, Sohu is profitable, and Changyou is losing money. In the past ten quarters, the net profit trends of Sohu and Changyou were exactly the same.

Changyou is a magic blanket, covered outside, and Zhang Chaoyang plays portal, video and search inside.

However, although Changyou has been listed for a long time, it is difficult to go ashore that day. We should not only continue to invest, but also pray that the things we make will be loved by others. From the past ten quarters, the living environment of the game business tends to deteriorate. R&D and market investment are getting higher and higher, and the profit space is narrowing rapidly.

In the second quarter of 2014, Sohu’s revenue reached a record $400 million, but it suffered a quarterly loss. The key reason is that swimming in this blanket is almost impossible to hide.

Changyou and sogou both need to invest more, but Sohu has married them off and can’t wait to get "quick money". If it’s to invest in videos, I’m afraid it’s also to dress up and receive a "bride price".

"Begging for fields and asking for homes, afraid of being ashamed to see them, Liu Lang is talented."

Zhang Chaoyang’s spare no effort in capital operation is not so much to raise funds for games and search business as to avoid potential risks, and it is based on the principle of "pretty girls get married first". How can it be listed if it is not beautiful, and can it be seen by Ali and Tencent?

Games, search, social networking, video … Sohu is involved in a wide range of fields, but no business has achieved success commensurate with its "Jianghu generations". Against the background of those Internet companies that started later than Sohu and grew several times and dozens times faster than Sohu, with a market value of tens of billions and hundreds of billions of dollars, Sohu’s ability of "seeking land and asking for homes" is particularly prominent.

In 2007, Sohu spent $35.3 million to purchase 18,300 square meters of office space in Tsinghua Science Park. In 2009, US$ 162 million bought 41,300 square meters of office space on Zhichun Road. Changyou did not show weakness. In 2009, it bought 15,000 square meters for $33.4 million, and in 2010, it bought 57,000 square meters for $171 million. More than 400 million dollars of high-quality real estate purchased in the core area of Zhongguancun, the valuation has already exceeded 1 billion dollars.

At present, Sohu and Changyou have rented over 30,000 square meters of office space in Beijing. If you don’t have the property you bought in the early years, you have to rent more than 100,000 square meters, and rent 8 yuan every day per square meter, with an annual rent of about 400 million. In the future, if Sohu stops all business and only eats rent, it will earn 1 million yuan a day! Sitting on more than 100,000 square meters of real estate worth five or six billion yuan, Zhang Chaoyang is very practical.

Buying a house in the core area of Zhongguancun is a shrewd investment for the coal boss. But after starting a business, only a few good houses are left behind, and it is not in vain for a lifetime! Even onlookers can’t help feeling sorry for Zhang Chaoyang.

Zhang Chaoyang is an Internet veteran in China. He made a name for himself early, but his success gave him a heavy burden: he was afraid of losing face and losing everything. He is not short of knowledge, ability or funds, but last stand’s courage. "Let’s talk about the new business" and "Is it risky? Give it to BAT! " . The leading brother is not enterprising, the elite soldiers will leave, and the people left behind will not focus on products but power … No wonder some people joked to take stock of "those opportunities that Zhang Chaoyang missed".

At the end of 2013, Sohu’s net assets reached $1.84 billion, and they were all very high-quality assets, of which cash and cash were $1.29 billion. If several properties in Zhongguancun are revalued, it will be many times more than the purchase cost before 2010. Together with Changyou’s equity, Sohu’s "tangible assets" are worth nearly $3 billion, while Sohu’s market value on Nasdaq is only $2.13 billion. Isn’t it that Sohu’s portal, video and search are worthless?(Note: tangible assets should be selected first, such as cash, real estate, holding stocks of other companies, etc.). Then, treat the company as if there is no tangible assets, and use free cash flow discount and other methods to value the business)

JD.COM’s valuation of nearly $40 billion is a bit high. But there is no love and hate for no reason, and there is no overestimation and underestimation for no reason. Liu Qiangdong earned a small sum of money, instead of buying a house or land, he circled more than 2 billion dollars and smashed it into his own direction. Although it’s too risky, the brave have won in ancient times, not to mention today. There is a sentence in Xin Qiji’s "Shui Long Yin Deng Jian Kang’s Feast Pavilion" that is very suitable for Zhang Chaoyang: "I am afraid that I should be ashamed to see Liu Lang’s talent. Unfortunately, the years are fleeting, the wind and rain are sad, and the trees are still like this! " # How can a man be as good as a tree #